Distribution Intel May 4: Hard Lemonade Is Moving Cases. Everything Else Is Adjusting.

Hard lemonade RTDs are displacing mainstream beverages at tsunami scale. Major retailers reallocating shelf space to THC, high-ABV, and non-alc. Crazy Mountain raises $15M. Lord Hobo outsources production. Premium bourbon grows while spirits decline. Capital and shelf space consolidatin...

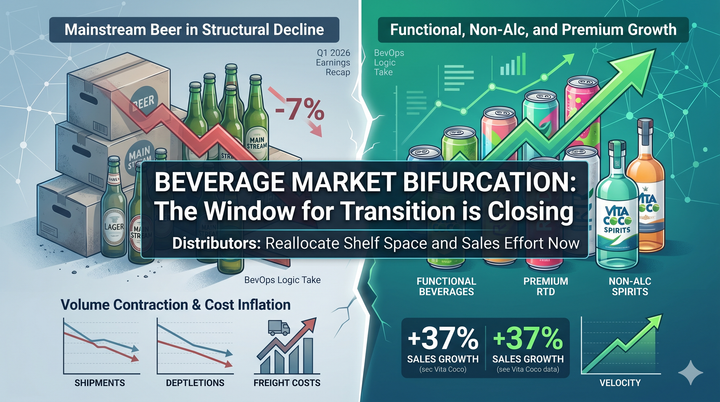

Three separate signals converged this week, and they all point the same direction. Hard lemonade RTDs are growing at tsunami velocity, systematically displacing mainstream beverage categories from retail shelves. Major bev-alc chains are executing coordinated shelf-space reallocation toward THC, high-ABV RTDs, and non-alc options. And institutional capital is funding venture-backed NA and functional beverage brands at scale. The pattern is not cyclical. It is structural. Regional distributors who are not positioned in hard lemonade, THC-adjacent, and functional beverage categories right now are losing incremental share to competitors who are. The 90-day window to build supplier relationships and sales infrastructure is closing.

Hard Lemonade RTDs Are Experiencing Tsunami-Level Growth

Source: BevNET, May 4, 2026

According to analysis from Bump Williams Consulting, hard lemonade ready-to-drink beverages are expanding at tsunami scale and systematically displacing mainstream RTD categories on retail shelves. The growth trajectory for hard lemonade exceeds that of hard tea, making it the primary driver of RTD category reallocation in 2026.

BevOps Logic Take: Hard lemonade is not capturing incremental shelf space. It is displacing existing categories. When a single RTD subcategory is described as a "tsunami," the implication is that retailers are pulling linear feet from adjacent categories to accommodate velocity. Hard lemonade is winning because it threads multiple consumer signals: functional benefit (lemonade positioning), RTD convenience, and alcohol delivery. For distributors, this means hard lemonade suppliers are now table stakes. If you do not have credible hard lemonade capability in your portfolio, you are losing incremental velocity to competitors who do. For suppliers, hard lemonade is no longer optional. Brands without a hard lemonade SKU will face velocity pressure from retail buyers who are actively seeking the category. The suppliers who move hard lemonade volume fastest will lock in shelf position. The ones arriving late will struggle to establish facings.

Major Retailers Are Executing Coordinated Shelf-Space Reallocation

Source: Brewbound, May 4, 2026

Multiple major bev-alc retail chains are simultaneously expanding shelf space for hemp-derived THC beverages, non-alcoholic alternatives, and high-ABV ready-to-drink cocktails while pulling space from legacy categories. This is coordinated reallocation, not isolated promotional activity.

BevOps Logic Take: When multiple major retail chains execute the same planogram decision in a single week, you are watching structural reallocation. The space being opened for THC, high-ABV, and non-alc is zero-sum. It is coming from mainstream beer and wine. This validates the thesis we outlined in our analysis of how mainstream beer is losing structural share to functional and growth categories. The retail buyers have already decided. They are not testing the category. They are executing the shift. For distributors, the implication is urgent. If you do not have a credible THC program and non-alc program in place within 90 days, you will be servicing shrinking mainstream beer planograms while your competitors capture incremental shelf space in growth categories. For suppliers, retail consolidation around growth categories means the buyers are moving faster and expecting faster response from distribution. The suppliers who can move velocity and drive compliance will win shelf space. The ones asking distributors to build capability on spec will lose.

Crazy Mountain Raises $15M, Signaling Venture Capital Conviction in NA Beer

Source: Brewbound, May 4, 2026

Celebrity-backed non-alcoholic beer brand Crazy Mountain closed a $15 million seed round from CAVU Consumer Partners just two months after market entry. The funding positions the brand to build national distribution, professional sales infrastructure, and marketing support at scale.

BevOps Logic Take: A $15 million seed round for a two-month-old NA beer brand is institutional capital validation that NA beer will capture material shelf space and volume. CAVU's investment thesis is straightforward: retail shelf space is opening for NA. Brands with venture funding and professional operational infrastructure will move faster than bootstrap or private-equity-backed competitors. For distributors, this means venture-backed NA suppliers will arrive in your territory with professional sales teams and account-level performance expectations. They are not asking permission. They are building distribution on a timeline. For suppliers without access to venture capital, the competitive pressure is immediate. Venture-backed competitors will outpace bootstrap brands in sales infrastructure, marketing spend, and account-level velocity tracking. The suppliers who do not have access to similar capital will find themselves defending turf against better-capitalized competitors.

Lord Hobo and Lone Pine Outsource Production to Isle Brewers Guild

Source: Brewbound, May 4, 2026

Evergreen Collective, the parent company of Lord Hobo and Lone Pine, is shifting production to Isle Brewers Guild in Pawtucket, Rhode Island. The move signals a strategic pivot away from owned brewing infrastructure toward a contract manufacturing model, with Evergreen's attention turning toward hospitality and beyond-beer innovation.

BevOps Logic Take: When a craft brewery best known for Boom Sauce goes quiet on the production floor, it is not a cost-cutting story. It is a capital reallocation story. Evergreen Collective is making a calculated bet: own the brand and the consumer relationship, outsource the tanks. Contract brewing via Isle Brewers Guild frees capex that would otherwise be locked in equipment maintenance, raw material procurement, and production labor. That freed capital gets redeployed into hospitality and beyond-beer innovation, two categories with meaningfully higher margin ceilings than packaged craft beer. For distributors, the practical implication is supply chain scrutiny. Contract-brewed SKUs can introduce lead time variability, quality control inconsistency, and packaging complexity. Distributor partners should get explicit commitments on production timelines and QC protocols before building inventory positions around Evergreen brands. For suppliers, the contract brewing model is increasingly viable as IBG and similar platforms scale capacity. The brand-asset model, own the consumer, outsource the manufacturing — is becoming the dominant playbook for mid-tier craft breweries that cannot compete on production scale alone.

MGP's Penelope Bourbon Grows 10% While Spirits Portfolio Declines 8%

Source: Shanken News Daily, May 4, 2026

MGP Ingredients reported that its Branded Spirits segment declined 8% to $44 million in Q1 FY2026. However, Penelope Bourbon, the company's flagship premium brand, grew 10% despite broader category headwinds. The performance gap reveals that growth is concentrating in premium-positioned spirits with direct consumer relationships.

BevOps Logic Take: When a single brand grows 10% while its parent company's spirits portfolio declines 8%, growth is concentrating in premium, heritage-positioned brands. Penelope is a premium bourbon with on-premise velocity and direct-to-consumer relationships. The rest of MGP's portfolio is wholesale-dependent and experiencing category headwinds. For distributors, this signals that spirits growth is now segmented. Premium, heritage-positioned bourbons are growing. Commodity-priced bourbon is not. The suppliers who are consolidating around premium bourbon positioning will grow. The ones competing on price will face margin compression. For suppliers, the message is unambiguous. Build brand equity, invest in direct consumer relationships and on-premise presence, and compete on positioning, not price. The distributors and suppliers who cede the premium segment to larger players will find themselves managing volume decline in commodity categories.

Key Takeaways

- Hard lemonade RTDs are displacing mainstream beer and RTD categories on retail shelves at tsunami scale. This is structural reallocation, not incremental growth.

- Major retailers are executing coordinated shelf-space reallocation toward THC, high-ABV RTDs, and non-alc beverages. Mainstream beer and wine are losing linear feet.

- Evergreen Collective's production outsource to Isle Brewers Guild is a capital reallocation play, not a cost cut. The brand-asset model is becoming craft brewing's dominant playbook.

- Venture-backed NA beer brands arrive with professional sales infrastructure and capital. Bootstrap and private-equity-backed brands face competitive pressure.

- Premium spirits are growing while commodity spirits decline. Growth is concentrating in heritage-positioned brands with direct consumer relationships.

The convergence of hard lemonade velocity, retail shelf-space reallocation, venture-backed brand funding, contract brewing consolidation, and premium spirits concentration is not random. It is a market signal. The suppliers and distributors positioned in growth categories now will own the three-tier system of 2027. The ones waiting will be managing decline.