Distribution Intel: The Reckoning. Mainstream Beer Is Dying. What's Next?

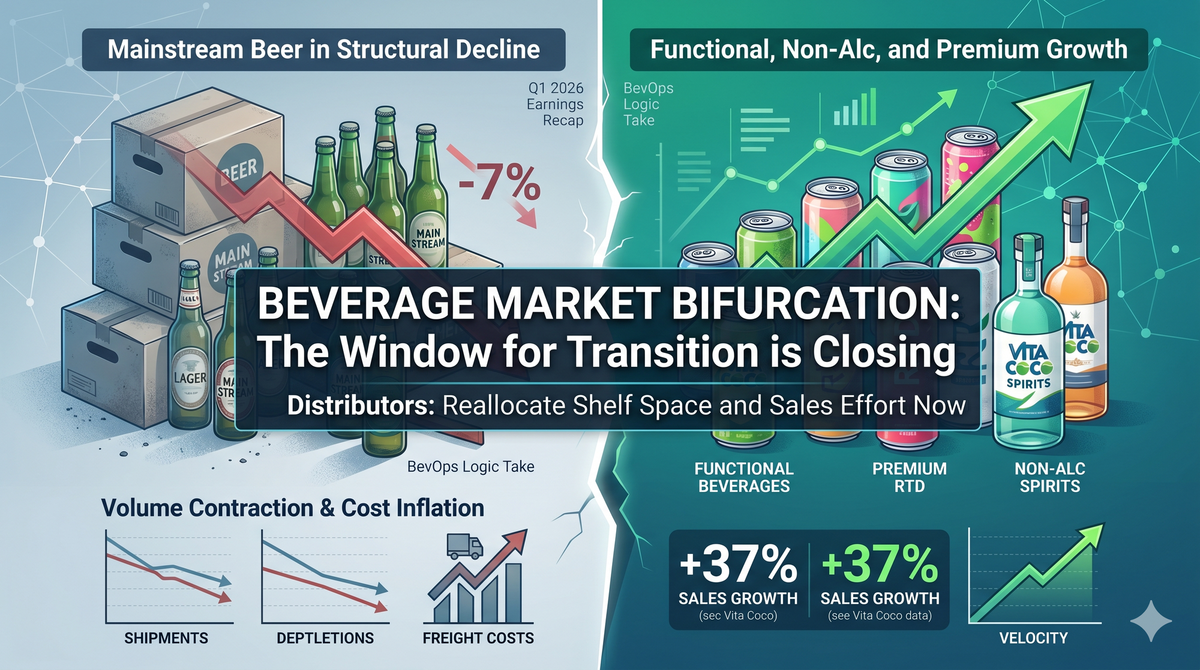

Mainstream beer is in structural decline. Boston Beer down 6.9%. Molson Coors posting volume losses. Meanwhile Vita Coco up 37% and Sazerac consolidating premium spirits. Regional distributors have a 90-day window to read the shift. Here's what the numbers mean for supply chain execs.

By Jason Gotcher | BevOps Logic

We've had three weeks of earnings data, and the pattern is unmistakable. Boston Beer down 6.9% shipments. Molson Coors posting single-digit volume declines with core brand weakness. Mainstream beer is in structural decline, and no amount of marketing spend or product innovation is reversing it. Meanwhile, functional beverages (Vita Coco up 37%), non-alc spirits (St. Agrestis acquired), and premium RTD are moving velocity. Sazerac is consolidating around tequila. RNDC is liquidating. The market is bifurcating into scale players (Coca-Cola, Sazerac) and specialists (functional, non-alc, premium). For regional distributors, the message is brutal: reallocate shelf space and sales effort now, or watch your margins compress into irrelevance over the next 12 months. The window for gradual transition is closing.

Boston Beer Q1 2026: Depletions -4%, Shipments -6.9%; Freight Costs Up $2.5M

Brewbound, April 30

Samuel Adams' parent company posted -6.9% shipments and -4% depletions in Q1 2026, with net revenue declining 4.4% to $433.9 million. Freight costs spiked $2.5M year-over-year, compressing margins on a shrinking volume base. This isn't cyclical weakness. The brand's core consumer base is trading craft beer for other categories.

BevOps Logic Take: For regional distributors carrying Boston Beer, this is a signal to rationalize SKUs and reallocate shelf space. Volume contraction paired with cost inflation means per-case profitability is deteriorating. Q2 earnings will show whether this is stabilizing or accelerating. If depletions remain negative, expect aggressive distributor consolidation and brand rationalization across mainstream craft.

Molson Coors Sees Core Brand Weakness in Q1; Single-Digit Volume Declines; Paid $275M for Atomic Brands

Brewbound, April 30

Molson Coors posted single-digit volume declines in Q1 with core brands Coors Light and Miller Lite bleeding velocity. Net sales grew 2% to $2.351 billion, but that growth masks a fundamental problem: legacy beer is contracting, forcing the company to spend $275M on Atomic Brands to find growth in adjacent categories. The return of Keystone Ice signals desperation in the value segment.

BevOps Logic Take: This is portfolio triage. When a company the size of Molson Coors is buying into new categories and reintroducing value brands, it means core beer can't hold velocity on its own. For regional wholesalers, this creates an opportunity to drop underperforming SKUs and reallocate that sales bandwidth to growth categories where turnover is faster and margins are better protected.

Vita Coco Sales Rise 37% in Q1

BevNET, April 30

Vita Coco posted 37% net sales growth to $180 million in Q1 2026, driven by retail expansion, improved pricing, and positive private label shipments. The coconut water brand's velocity stands in direct contrast to mainstream beer's contraction. Consumers are shifting from commodity beverages to functional products with perceived health benefits.

BevOps Logic Take: A 37% growth rate in a mature beverage category is rare and durable. If Vita Coco is executing this consistently, it's proof that functional beverages are capturing wallet share from beer and juice. Regional distributors should be aggressively stocking functional categories and building direct relationships with retailers. This isn't a niche anymore. It's where velocity lives.

The Wine Group Acquires Phony Negroni Maker St. Agrestis

Brewbound, April 29

The Wine Group acquired St. Agrestis, the top-selling non-alcoholic spirits RTD brand, for an undisclosed sum. Phony Negroni's 200mL bottled format is the leading product in the non-alc spirits segment according to Mintel. This acquisition signals that established beverage platforms now view non-alc spirits as a material growth vector worth deploying capital to acquire.

BevOps Logic Take: When major distributors start acquiring non-alc brands outright, the category has crossed from emerging to essential. Non-alc spirits RTD is moving velocity, commanding margin, and capturing consumers trading alcohol volume for functional benefits. If you're not carrying this category with dedicated shelf space and sales effort, you're leaving money on the table while competitors lock in customer relationships.

Sazerac Invests in Kendall Jenner's 818 Tequila for Nationwide Sales and Distribution Partnership

BevNET, April 28

Sazerac announced a strategic partnership with 818 Tequila, deploying its national distribution network to scale a premium tequila brand. This move consolidates Sazerac's position in the high-growth spirits category while 818 gains access to the industry's most efficient logistics infrastructure. It's a validation that spirits consolidation around scale is accelerating.

BevOps Logic Take: Sazerac backing 818 with capital and distribution muscle confirms that winning in spirits requires either national reach or hyperlocal dominance. Mid-tier regional distributors without scale are getting squeezed out of premium spirits. If you're a regional player, your choice is binary: align with a national spirits platform or build cult velocity in a niche where you own the market completely.

The math is now simple. Mainstream beer is in structural decline. Functional and non-alc categories are in structural growth. Scale consolidation (Coca-Cola, Sazerac) and category specialization are the only winning strategies. For regional distributors, the next 90 days are critical. Use this earnings cycle to rationalize your beer portfolio, redeploy sales bandwidth toward functional and non-alc categories, and begin building direct relationships with high-growth brands. The distributors who move now will capture growth. The ones who wait will be acquired at a discount or marginalized into irrelevance.